Preparing for college

Start saving for a promising future

Is your college funding on track?

Calculate how much you’ll need to put aside each month to afford the college of your choice.

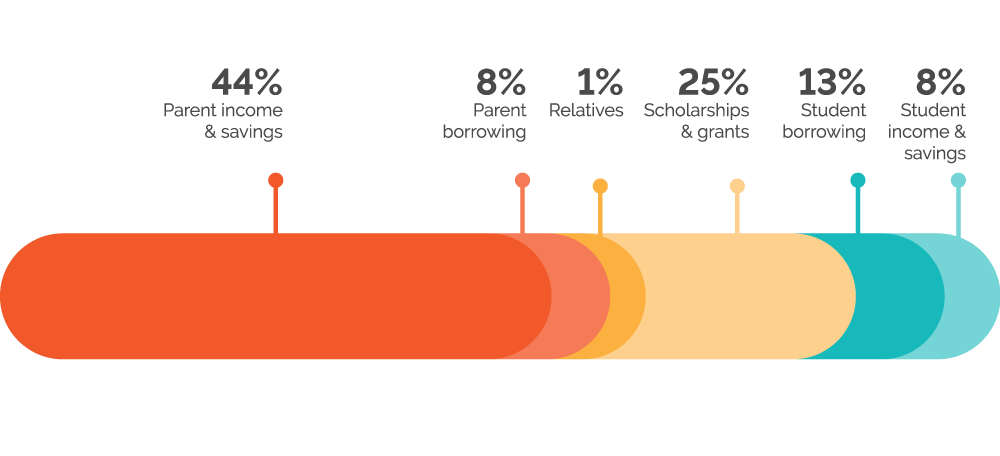

How America pays for college

Source: Sallie Mae. (2020). How America Pays for College 2020: What You Need to Know.