Understanding disability insurance: types, benefits, and options

Maintaining a steady income is pivotal to ensuring your financial stability and is intricately tied to overall well-being. However, a sudden loss of income can derail your current lifestyle and even your long-term financial goals, even for those who have an otherwise solid financial foundation.

While job loss is the obvious threat to income potential, another pervasive cause of reduced or lost income is disability, which affects millions of households each year, regardless of economic class.

U.S. adults live with some type of disability.

When it comes to disabling events, the “it won’t happen to me” myth creates a false sense of security, putting you and your family at risk. In reality, even if you don’t ever experience a lifelong disability, studies show that 20% of Americans have been out of work for an extended period in the last 10 years due to a condition, injury, or illness, and throughout an entire career, these odds only go up.1

Likewise, disabling events aren’t always catastrophic and they aren’t even always physical. Mental health-related disability claims have increased by 40% in the past five years.1

What’s more, lost income doesn’t only affect your ability to cover your immediate financial needs, but the longer you experience a disability leave, the bigger the impact it has on your financial wellness, including depleting emergency savings, lost investment opportunities, and reduced retirement readiness.

However, for those who have disability insurance coverage, the negative impact is far reduced.

Workers who lacked disability coverage at the time of their leave are nearly 50% more likely to say their leave had a major or devastating financial impact on their household.

Source: Guardian, (2022). Guardian’s 12th Annual Workplace Benefits Study.

Disability insurance offers a solid base for any financial strategy. Accidents, illnesses, and injuries can happen to anyone, but with disability insurance, you can rest easy knowing your lifestyle and future goals are protected.

Table of contents

- What is disability insurance?

- Who needs disability insurance?

- What are the types of disability insurance?

- What does disability insurance cost?

- How to get disability insurance

What is disability insurance?

Disability insurance: A type of insurance product that provides income if a policyholder is prevented from working and earning an income due to a disability.

Disability insurance provides the policyholder with income if they are not able to work due to a disabling event. Disabling events can be physical or mental illnesses or injuries, they can disrupt part or all of your job, and they can affect you between a few weeks up to 20 years or even until retirement age for some long-term disability policies. Some policies replace a percentage of your income—often between 60% and 80%—while others cover the full amount lost.

Who needs disability insurance?

When your income becomes unreliable, disability insurance is designed to help you meet your immediate financial needs while providing stability that keeps you on track for your long-term goals.

Since disability can affect anyone, it is important to know where income replacement may come from in the case of a disabling event.

What types of disability insurance are available?

Each disability is different as is each disability policy, so it is important to understand your many choices to ensure the right coverage at the right time.

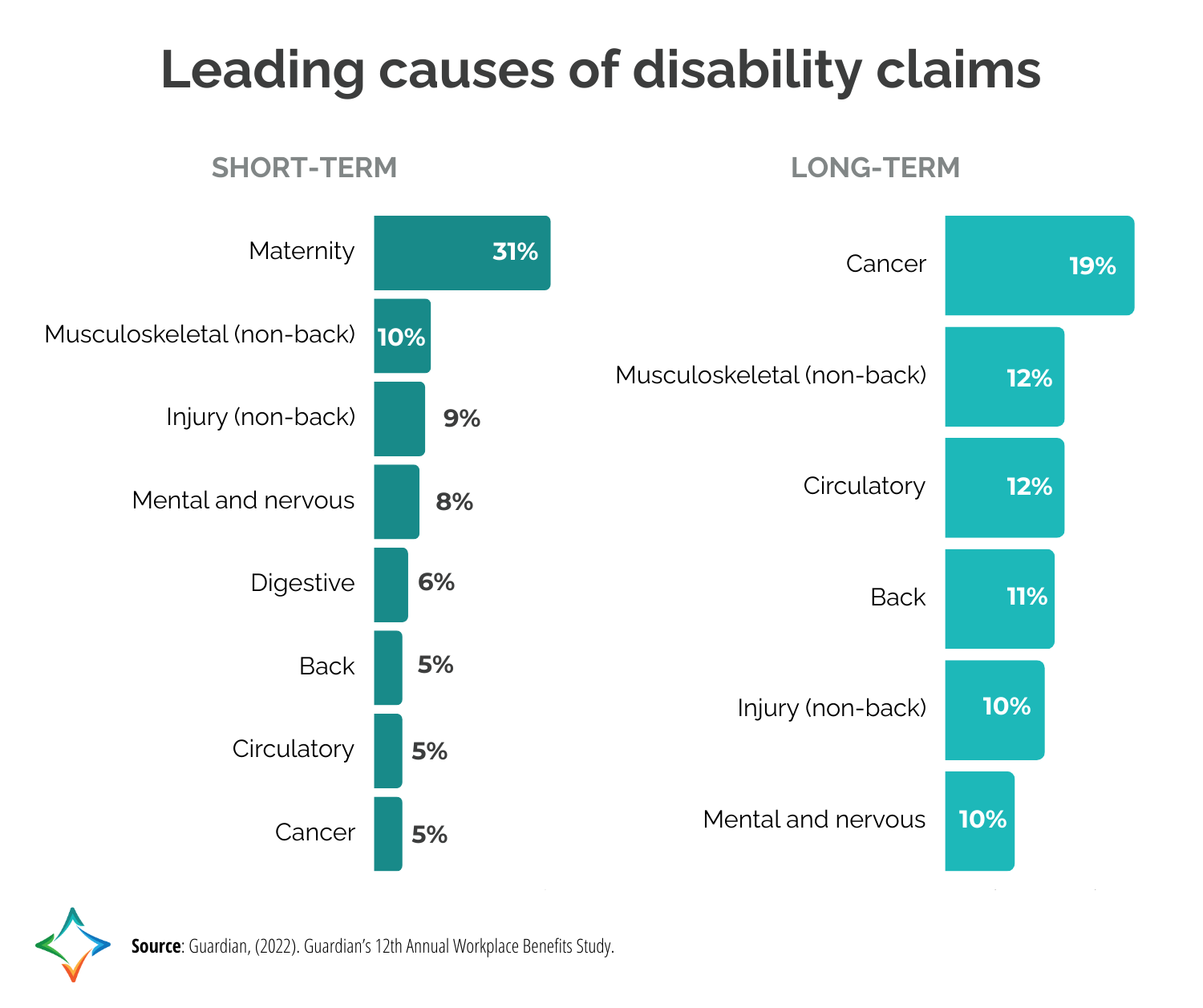

Short-term vs. long-term disability insurance

While every policy is different, they all fall into two broad categories: Short-Term Disability (STD) and Long-Term Disability (LTD). The biggest difference between short-term and long-term disability insurance is how long you’ll receive benefits if you’re unable to work.

As the name indicates, short-term policies are intended to cover you for a short period with a maximum benefit period of no more than two years. This contrasts with long-term policies, which have a maximum benefit period ranging from several years to the rest of your lifespan.

The other difference is the waiting period before benefits begin. Short-term disability policies typically begin paying within a couple of weeks from the qualifying illness or injury. For long-term policies, this longer waiting period—often called the “elimination period”—can take around 90 days.

Waiting period: The waiting period, or elimination period, is the amount of time you are unable to work before your disability insurance benefits begin.

Social Security benefits

In the U.S., you technically have access to Disability Insurance Benefits under Social Security, a federal program managed by the Social Security Administration (SSA). These benefits are designed to provide financial support to individuals and their eligible family members in case they are unable to work due to a qualifying medical condition.

These benefits are available without any action needed on your part. However, the coverage is limited. To be eligible for disability benefits, you must:

- Be unable to work because you have a medical condition that is expected to last at least one year or result in death.

- Not have a partial or short-term disability.

- Meet SSA’s definition of a disability.

- Be under the full retirement age.

It’s important to note these benefits do not cover disabilities under a year and will only kick in if you cannot reasonably do any job, not just your own job. Likewise, it will cover a percentage of your lost income, but never the full amount.

While Social Security is a helpful safety net for many, it should not be your primary plan for disability coverage.

Disability insurance through your employer

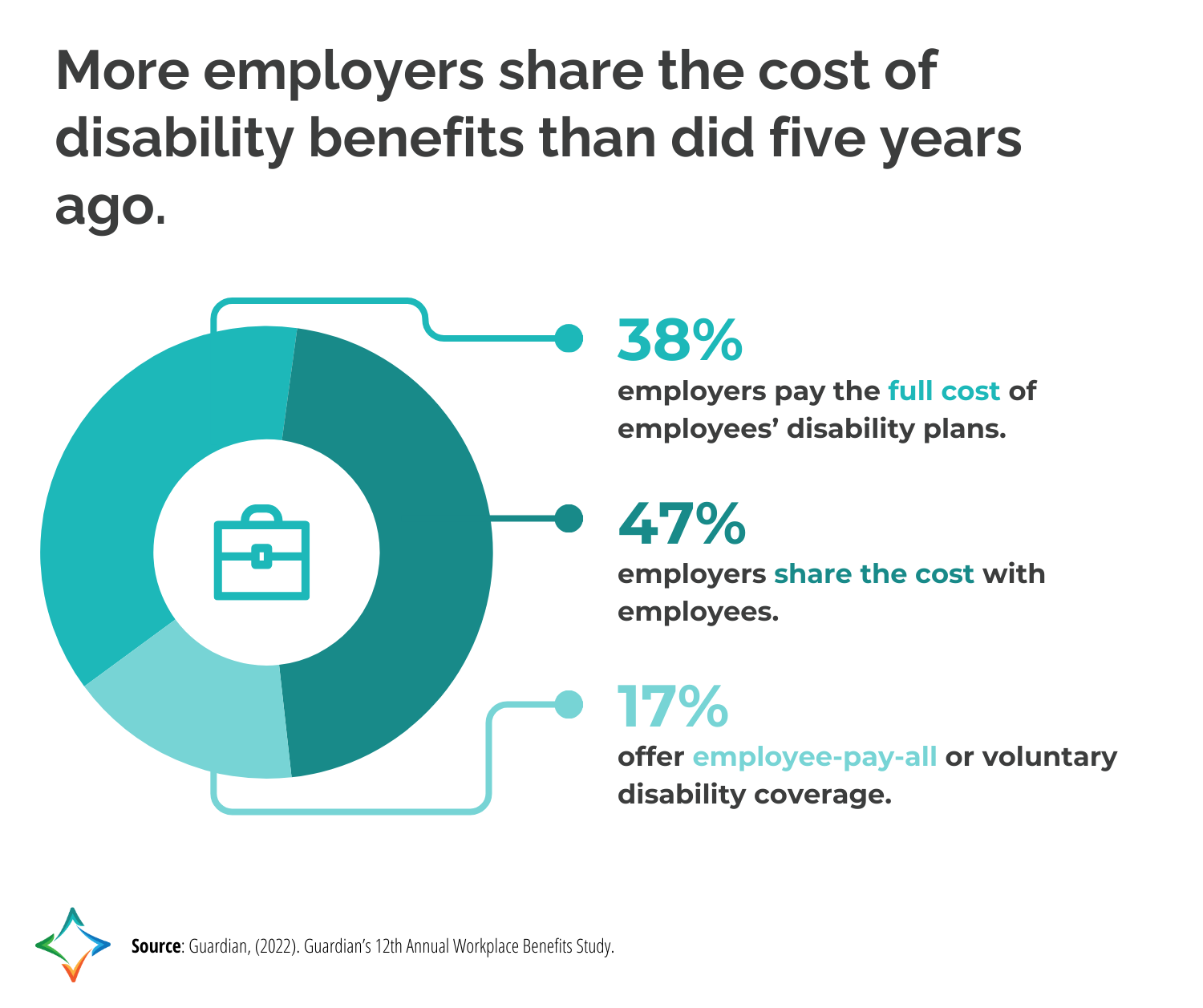

Fortunately, a majority of employers offer some form of disability insurance as part of their employee benefits package, with more offering short-term disability than long-term.1

However, like any benefit, how this is offered varies across companies. Of those businesses that offer disability coverage in their benefits packages, 47% share the cost of the policy with employees, 38% cover the full cost, and 17% offer it as a voluntary benefit that the employee must pay in full.1

Any group coverage your employer offers is better than nothing because it lessens your income gap if you were to become disabled. Still, it doesn’t completely eliminate your responsibility.

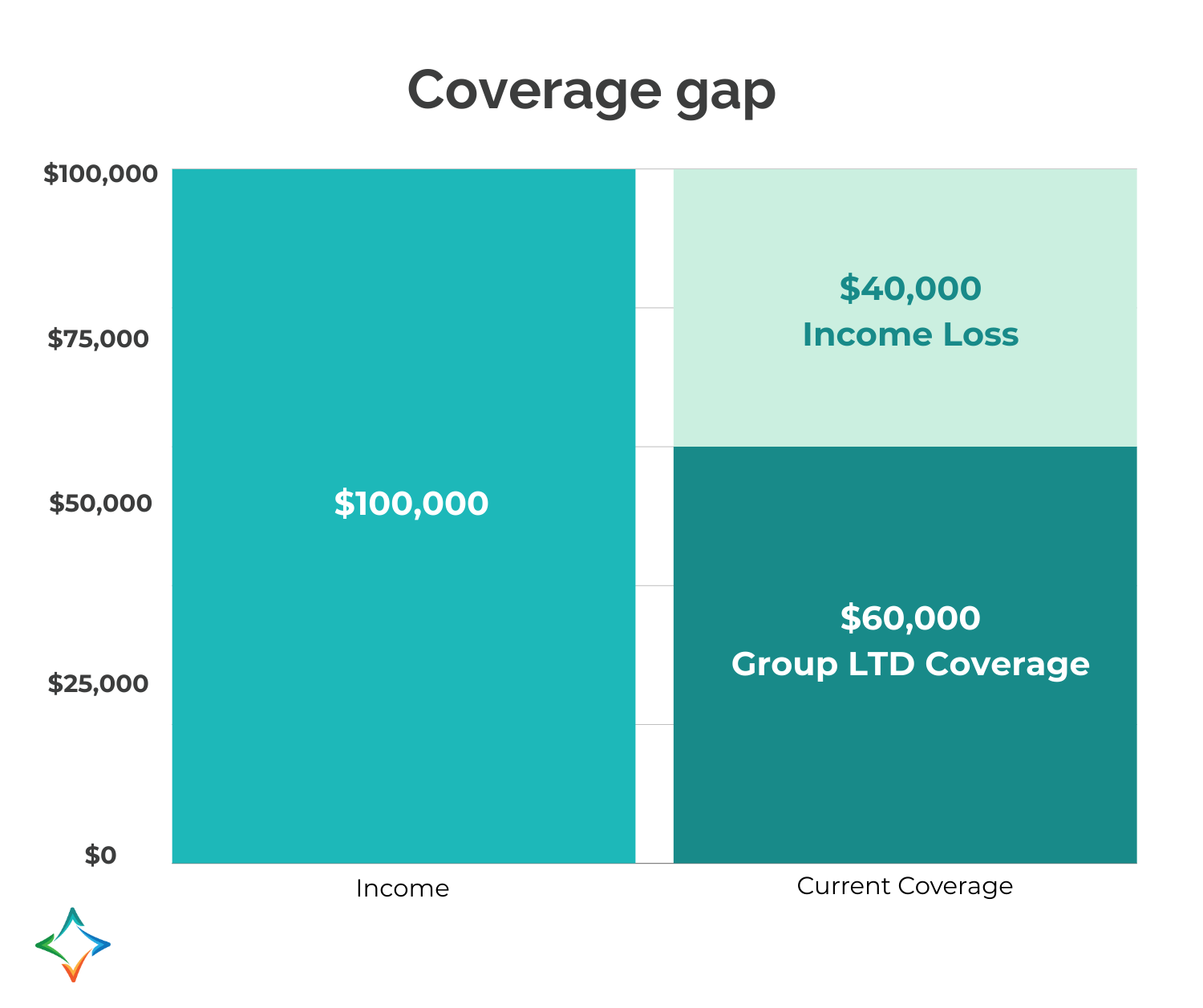

Take the following scenario for example: A young professional is making $100,000 a year with bonuses, and they have a standard 60% group LTD plan. As you see in the illustration below, their monthly paycheck drops significantly when relying solely on their group plan.

The employer disability benefit was never designed to take care of the employee entirely.

Supplemental disability insurance

When preparing properly for a disabling event, it takes coordination between group and privately-owned insurance to keep your finances in order and your goals on track.

Getting individual disability insurance is going to be your best bet to shore up your income gap while disabled, as well as providing you with options and flexibility in your benefits.

If your employer does not offer disability insurance or you are looking for supplemental coverage, you have a broad range of options from a variety of carriers.

Disability insurance coverage options

In addition to these two main types of disability insurance policies—short-term and long-term—you have several additional options to consider with coverage, usually referred to as riders:

- Noncancellable policy: This type of policy cannot be canceled should your health status change after begin paying a premium on your short-term or long-term insurance policy.

- Own occupation: This provides benefits if you are unable to perform the duties of your own occupation, rather than any occupation for which you might be suited based on education, training, or experience. This solution is highly recommended for professionals in high-paying specialized fields.

- Future increase option: This rider allows you to increase your coverage in the future without undergoing additional medical underwriting, typically subject to certain conditions.

- Cost of living adjustment (COLA): This increases your benefits over time based on the increase in the cost of living, as measured by the Consumer Price Index (CPI). Often, this add-on is in exchange for paying a higher total premium.

- Residual of partial disability rider: This allows you to return to work part-time and collect part of your salary if you are still partially disabled, without voiding your benefits.

- Return of premium: This requires the company to refund a part of your premium if no claims are made for a specified period, as outlined in the terms of the policy.

- Waiver of premium provision: This is a clause within the policy that removes any responsibility of payment toward the premium after you are disabled for 90 days.

- Catastrophic disability rider: This rider provides added benefits if you suffer a severe disability, such as the loss of multiple limbs or senses.

- Mental or nervous disorder limitation rider: Some policies may limit coverage for disabilities caused by mental or nervous disorders unless they meet certain criteria or are specifically covered by this rider. With mental or nervous claims making up 10% of all long-term disability claims, this is often worth asking your professional about.

What does disability insurance cost?

Since the primary role of a disability insurance policy is to replace your income, costs, or premiums, the typical starting range is 1% to 3% of your annual income. However, the actual cost will depend on the type of policy you choose and your specific situation.

For example, existing health factors will influence your monthly premium payments, including your age, smoking status, the demands of your occupation, and income level. Generally, higher earnings result in higher premiums to safeguard those earnings, as do risky careers where the likelihood of becoming disabled is greater.

Likewise, any riders or add-ons can incur a higher premium because of the benefits or flexibility they provide, including own-occupation policies that insure you even if you can work in a different role.

However, there are also ways to reduce costs, such as opting for a long-term policy with an extended elimination period.

How to get disability insurance

The best way to sort through your options and find a policy that works for you is to consult with an independent agent or advisor who can look at your full financial picture—from emergency savings and employee benefits to long-term goals and retirement—and help you shop a variety of policies and carriers to suit you and your family’s needs.

By taking this comprehensive approach, you can ensure you have the coverage you need while balancing the monthly premium payments with what you need for other financial goals.

Are you interested in exploring this further with a financial professional? North Star Resource Group has licensed professionals in every U.S. state who provide a holistic perspective on your financial life and work in tandem with our Disability Insurance experts to find creative solutions for any situation. Together, they can help you find the correct policy based on your income and needs.

Connect with us for personalized advice on disability insurance.

1Guardian, (2022). Guardian’s 12th Annual Workplace Benefits Study.