Did you ask these questions about your disability income policy?

If you work in a specialized field, you likely took a long road to get there.

Whether you’re a doctor, nurse, dentist, veterinarian, attorney, or a small business owner, you’ve put in a significant investment of time, money, and hard work to get to your career.

It’s all worth it when you consider the decades you’ll spend making a high income in your area of focus.

Unfortunately, while 20-30+ years in your career is likely, it’s not guaranteed.

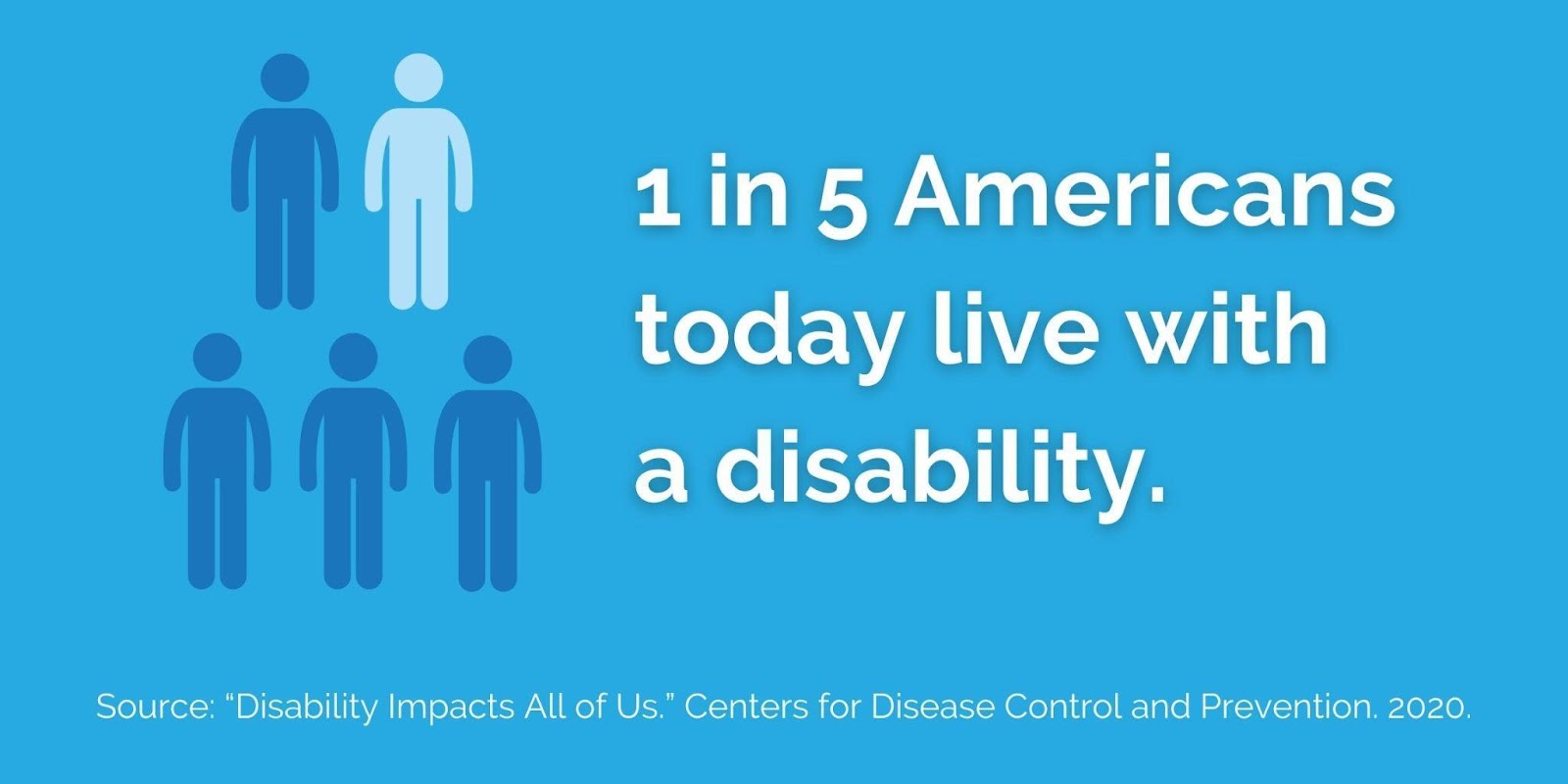

One out of five Americans today live with a disability, and it’s predicted this number will only go up as we study the effects of long-COVID (UC Davis Health, 2021).

But don’t worry.

Being too hurt or sick to work doesn’t need to derail your financial future. There is a precaution you can take to help protect your income, and it’s called disability insurance.

Disability income insurance replaces the income lost if you are too sick or injured to perform your job duties, and it’s essential in a well-balanced financial strategy.

Whether you’re looking to buy your first-ever disability policy or you’ve had insurance for years and need to reevaluate your coverage, the questions in this article can help.

What type of disability coverage do I need?

Every high-income professional should look into disability insurance. Even if your employer offers short-term options, you’ll likely want more coverage, especially during your core wealth-building years.

Luckily, there are a wide variety of coverage options so you can find the right policy and premium for your complete financial strategy. Still, all the options get complex, so let’s break down some of what you’ll be looking at:

How long will I receive benefits?

Short-term versus long-term

A short-term disability policy generally begins paying shortly after you become disabled and pays for a maximum of 3 to 12 months. This coverage can help cover monthly expenses while you can’t work.

However, short-term disability insurance does little for your long-term goals.

Enter long-term policies, which can pay monthly until you turn 65 or 67 while the disability persists. This income replacement allows you to continue to fund retirement and other financial goals.

Will my benefit cover income from my specialty or any position?

Any-occupation versus own-occupation

Within long-term disability insurance, you have the option of any-occupation and own-occupation.

Any-occupation disability insurance insures you only if you’re unable to work any job you’re reasonably qualified for, even if it’s at a much lower pay rate.

In contrast, own-occupation insures you against an inability to complete the specific job you have. As a specialized professional, this is likely going to give you the protection you want, even if the premium is higher.

Within these two major categories, you may also see options such as transitional own-occupation and modified own-occupation.

The idea here is to ask the questions about what kind of benefits you will get based on the type of work you are doing.

How can I personalize for my specific needs?

I want you to ask this question for every financial solution you consider, as they should ALL be personalized.

In disability insurance, you can personalize with riders: Add-on features of a DI policy that may or may not cost an additional premium.

A few examples of riders include:

- Partial or Residual Disability: Provides partial coverage if you can do some responsibilities of your job but not all of it, and it provides a partial benefit as you recover from your disability.

- Inflation Protection or Cost of Living (COLA): Increases your benefit amount over time to match inflation, which is valuable if you become disabled at a young age.

- Future Purchase Option: Allows you to buy a larger benefit later without an additional approval process.

- Catastrophic Disability: Provides a larger benefit if you are disabled beyond not being able to work, but unable to maintain any normal lifestyle.

- And more!

How can I possibly sort through all of this?

Remember who I said needed disability insurance? High-income, packed-schedule, hard-working specialized professionals.

AKA, people who don’t necessarily have time to wade through pages and pages of DI policy options.

Also, my primary clients.

I would love to schedule a phone call or meeting with you to talk about what you’re looking to get out of protecting your income. Our team of insurance specialists can then help you shop to find the one that matches your budget and needs or confirm that you have the right coverage for you.

Email me to set a date in the calendar!

Download our free, no-obligation Job Transition Checklist!

|

Author: James Jaderborg, CLU®, ChFC®

James Jaderborg specializes in working with business owners, physicians, and medical professionals to help them overcome financial challenges unique to their careers.

4715830IR/DOFU 5-2022