How to Balance Your Retirement Strategy to Maximize Growth and Minimize Taxes

Author: James Jaderborg, CLU®, ChFC®

James Jaderborg specializes in working with business owners, physicians, and medical professionals to help them overcome financial challenges unique to their careers.

Ask 100 people about their retirement lifestyle plans and you’ll get 100 different answers.

Spend more time with family. Travel. Pursue a hobby. Start a business.

Then, ask them their biggest retirement fear, and the answers quickly narrow down:

To have enough money to live how I want through the rest of my life.

You see, while retirement lifestyle and the dollar amount representing “enough money” is going to be different for everyone, we all have this same central desire of enough—enough to be comfortable, happy, and fulfilled.

The best way to get enough in retirement investing? Maximize growth for the money you put in and minimize taxes as it grows and when you take it out.

In this article, we will walk through how a balanced retirement strategy achieves both of these objectives.

Then, when you understand the why, what, and how of smart retirement investing, you can ask your financial professional important questions to build a strategy that works.

To make this super attainable, I’ll also provide you with a list of questions that you can bring to meetings with a financial professional and that you can use to help you take the reins on your retirement future.

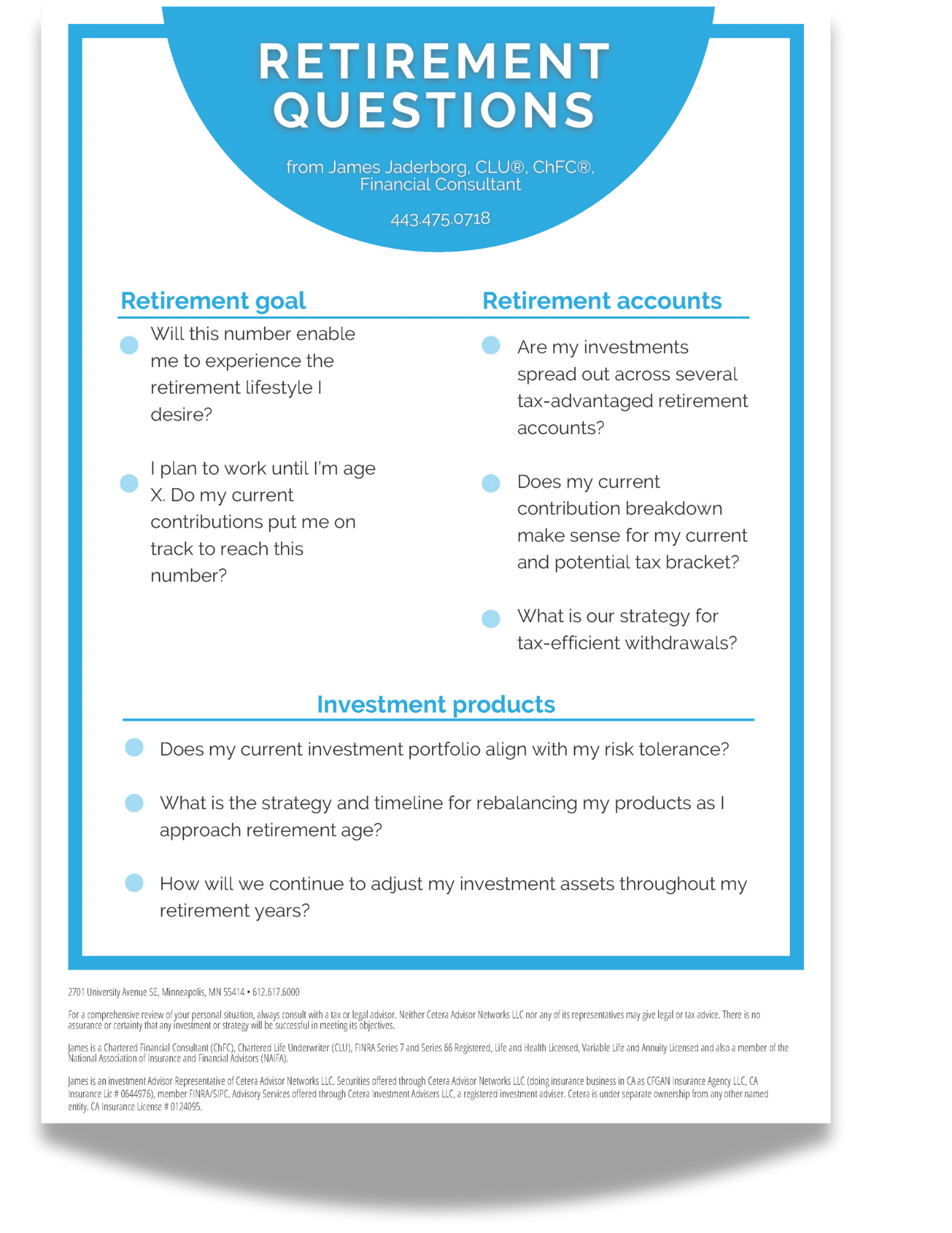

Talking Point: What’s my retirement number?

How much do you need to retire well? Use our calculator to find out!

Then, you can bring that number to your financial professional with these additional questions:

- Will this number enable me to experience the retirement lifestyle I desire?

- I plan to work until I’m age X. Do my current contributions put me on track to save this number?

What does a balanced retirement strategy mean?

When a financial professional says you need a balanced investing strategy, they are usually referring to balance in account types and investment products.

Investment accounts are where you invest (IRA, 401(k), 403(b), Health Savings Account, etc.), and a product is how you invest within those accounts (stocks, bonds, CDs, mutual funds, ETFs, etc.). Typically, you will have several options of products within a specific account.

How does differentiation in accounts and products lead to a balanced investing approach?

Remember, our goal in investing is to maximize growth on the money you put in and minimize taxes as it grows and when you take it out.

With any investment strategy, you will see some dips and peaks in returns. However, with a diverse product mix of stocks, mutual funds, ETFs, and more, those dips and peaks should balance out and result in an overall upward motion of your investment total. Balancing products helps you maximize this growth.

Then, when it comes to investing accounts, each one has different tax implications. Some accounts tax contributions and some tax withdrawals; some tax growth some grow tax-free or tax-deferred.

Just like with products, when you balance your investing accounts or “buckets,” you become intentional about these tax implications and make them work for you.

Balancing your retirement investment accounts to minimize taxes

Let’s breakdown the main retirement investing accounts to see what those tax implications are and how you may use them in your overall strategy:

Pre-Tax Accounts

Traditional IRA, 401(k), 403(b), 457, 401(a), SIMPLE IRA, SEP IRA

With pre-tax, or deferred-tax accounts, your contributions go in before any taxes are taken out. Additionally, as the money grows in value, you don’t pay taxes on the returns.

When you’re ready to retire and start using the money you’ve invested, those withdrawals, otherwise known as distributions, will be taxed as income.

For those whose income will go down in retirement, this is a way to defer those taxes until you’re at a lower tax rate. Also, your money has the potential to grow more substantially because you are putting a higher dollar amount in at the beginning.

However, the flip side of this is that your total retirement contributions will need to account for the taxes you’ll incur with every withdrawal.

If all your retirement contributions are in a traditional account, you’d need to withdraw a few thousand dollars extra from your retirement funds each year to pay your taxes and have enough to live on.

Post-Tax Accounts

Roth IRA, Roth 401(k), Roth 403(b)

With a Roth IRA or 401(k) or any post-tax retirement account, your contributions are made with after-tax dollars and then grow tax-free. Then, in retirement, all qualified withdrawals1 can be made tax-free.

A benefit of these accounts is that, since you have already paid taxes on the dollars invested, your distributions will all go into your pocket, regardless of your current tax-bracket.

1Qualified distributions must meet a five-year holding period and satisfy one of three additional requirements: Reaching 59 ½, disability, or death. Five years is measured from January 1 of the year of your first Roth contribution.

Taxable Accounts

Bank accounts, brokerage accounts, and other investments

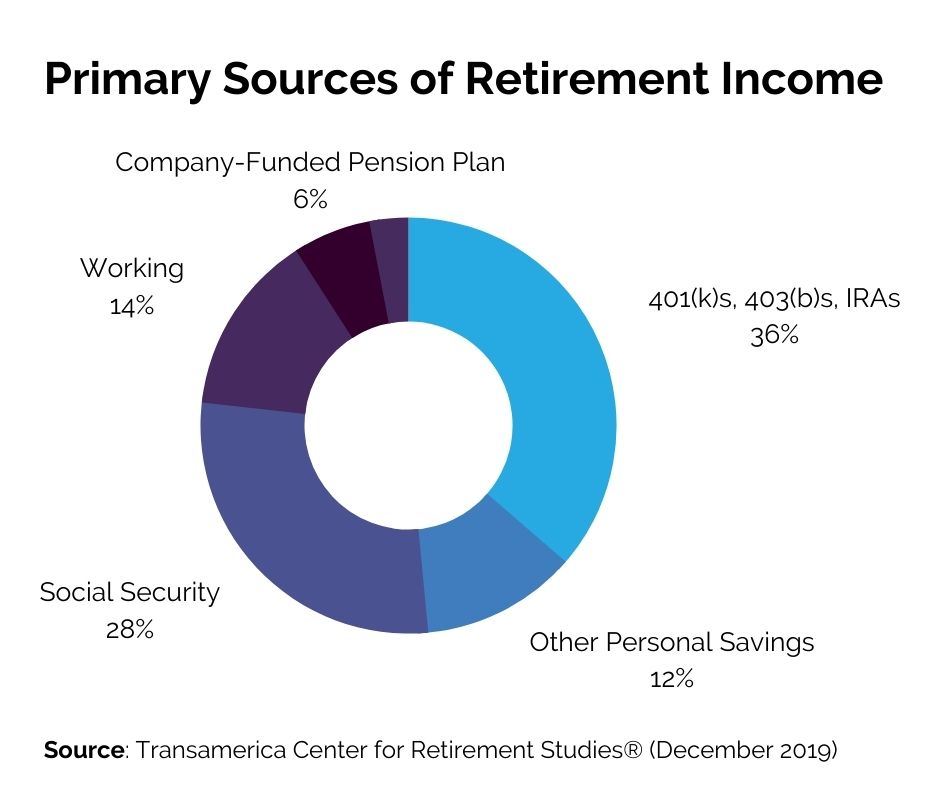

Remember the chart above that showed the average American using personal savings for 12% of their retirement funding (Transamerica Center for Retirement Studies®, December 2019)?

Contributions to personal savings and investments accounts are made with after-tax dollars and are taxed on their net capital gains and qualified dividends, albeit often at a preferential rate. Additionally, you may pay a long-term capital gains tax in brokerage accounts when you sell and withdraw a stock you’ve held for over a year.

Based on all these taxes, you may wonder why anyone would save in these accounts over a tax-advantages retirement account. There are two core advantages:

- Flexibility. If you want to withdraw from a pre-tax or post-tax retirement account, the IRS has a whole list of qualifiers you need to meet to avoid fees and a hefty tax bill (most qualifications have to do with age). In a personal savings account, you don’t have the restrictions, if you absolutely need the money, you can withdraw it early.

- Contribution limits. Retirement accounts have annual contribution limits, and for high-income individuals or those looking to seriously invest, you can run up against these limits before you know it. A taxable account may be a solution if you want to invest more toward your golden years and have already maxed out your 401(k) or IRA.

Other retirement funding strategies to consider:

Health Savings Accounts (HSA)

A health savings account is a tax-advantaged medical savings account for those enrolled in a high-deductible health plan. The contributions to an HSA are made without tax and grows tax-deferred.

You can use money in an HSA at any time for qualified medical expenses and it will not be taxed as income. Alternatively, you have the option to save and invest the money in this account and withdraw it after age 65 as taxed retirement income for any expense.

If you are on a high-deductible health plan, it may be worth talking to your financial professional about if an HSA could be part of your retirement strategy.

Hybrid Long-Term Care Insurance and Medicare Supplement

One of the primary concerns for those entering retirement is medical costs (Transamerica Center for Retirement Studies®, Dec. 2019). As you age, these costs go up and become unpredictable, both of which can have a strain on your planned retirement distributions.

Although not retirement investing, hybrid long-term care and Medicare supplement coverage are both methods to reduce medical costs in retirement, thereby allowing your investments to last longer into your golden years.

A comprehensive financial professional should be able to walk you through how to coordinate these products with your overall retirement strategy if you ask.

READ MORE: Are you managing the second most significant risk to a happy, fulfilling retirement

Talking Point: What retirement accounts are appropriate for me?

To start rebalancing your retirement savings buckets, you first need to know what buckets you have. If you haven’t consolidated accounts from previous employers, now is a good time to consider that as well.

Then, ask your financial professional these questions?

- Are my investments spread out across several tax-advantaged retirement accounts?

- Does my current contribution breakdown make sense for my current and potential tax bracket?

- What is our strategy for tax-efficient withdrawals?

Diversifying your investment products to maximize growth

With most retirement accounts you choose, you will have some flexibility on the investment products you work with within those accounts.

With any investment strategy, you will see some dips and peaks in returns. However, when you and your financial professional properly diversify your mix of stocks, mutual funds, ETFs, and more, you do so with the hope that those dips and peaks should balance out and result in an overall upward motion of your investment total.

But what does a diverse portfolio actually mean?

First, it’s NOT simply owning a bunch of different stocks, but only owning stocks. Stocks are only one product, and while owning a lot of different ones protects you if one single company tanks, if the entire stock market crashes, you are still in trouble.

You want to balance your entire investment portfolio: Some stocks, some mutual funds, some ETFs, and more and then diversifying within those product categories as well.

This is also referred to as asset allocation, and it means you are investing in a variety of vehicles that don’t move parallel to each other. When one goes down, another may go up—managing risk for you in the long-term and preparing you to shift short-term over time.

It sounds complex, and it can be, but if you are working with a financial professional who is dedicated to you understanding your own investments, they should have meetings set up to walk you through the whole thing.

Talking Point: What investment products do I own?

If you’re investing with a financial professional, they likely have some product diversification set up for you in your accounts. However, this is also determined by your target retirement date, risk tolerance, and personal preferences, which they can only know through talking to you.

If you haven’t talked about it recently, it may be worth bringing up a few asset allocation questions in your next meeting:

- Does my current investment portfolio align with my risk tolerance?

- What is the strategy and timeline for rebalancing my products as I approach retirement age?

- How will we continue to adjust my investment assets throughout my retirement years?

Why rebalancing your retirement investments is an important move right now

In this article, we examined what it looks like to take a truly balanced approach to retirement investing, and we learned it is a layered strategy of accounts, products, and categories within products all of which have tax and growth implications.

It kind of makes you wish you could just dump it all into one account and not worry about it, doesn’t it?

But retirement investing is one of the most important financial decisions you can make in life. It’s what is going to enable you to save enough money to live how you want to through the rest of your life—and what’s more important than that?

Financial professionals recommend a balanced retirement strategy because we know inflation, the markets, and taxes are all unpredictable, and diversity helps us overcome this volatility to minimize taxes and maximize growth in the long-term.

But we also know YOU are predictable.

The more consistent, level-headed, and balanced you are in your investing, the more likely you are to weather these external ups and downs.

Once you decide it’s time to rebalance, keep in mind that moving all that money around will have some current tax implications as well. I highly recommend getting a financial professional on board—even if it’s just a one-time consultation—to help you create the balance thoughtfully and over time to get your overall investment strategy on track.

If you don’t have a financial professional in your corner already or if you’re looking for a second opinion, I am here and happy to help.

|

Download our free, no-obligation list of retirement preparation questions!

|

Neither asset allocation nor diversification guarantee against loss. They are methods used to manage risk.

Financial professionals do not provide tax or legal advice and this should not be considered as such. Please consult a tax or legal professional for advice regarding your specific situation.